Extended Producer Responsibility | All you need to know

Here is your handy guide to all things Extended Producer Responsibility (EPR). Find out what you need to know, including why it’s important, whether it applies to you, timelines, what to do and much more.

Contents

- Why EPR is important?

- What are modulated fees?

- EPR timeline

- Why is EPR being implemented?

- Does EPR affect your business?

- How much will EPR cost?

- When to collect and report your data for 2023

- How to comply with EPR

- When will EPR officially start, and what will the waste management fees for 2024 be?

- What data will you need to collect?

- Reporting your data

What is EPR?

Extended Producer Responsibility (EPR) is a new UK legislation that will replace the current Packaging Waste Regulations with the data collection phase starting in 2023 and a phased introduction of the fees from 2024. It is an environmental policy that requires producers to pay the total cost of dealing with the waste they produce from when it is placed packaging onto the market to the end of its life.

These new regulations build on the existing Packaging Waste Regulations, which have been in place since 1997, and it is hoped that their implementation will reduce the environmental impact of packaging. The idea is similar to other environmental legislation in the principle of Producer Pays. So, under EPR proposals, packaging producers will be responsible for the entire cost of recycling the household packaging they place on the market, including the cost of collection, treatment, and recycling minus the value received for the recycled material.

UPDATE: The first two packaging EPR reporting deadlines for large producers remain unchanged; however, no enforcement action will be taken if they are submitted by May 31 2024.

Defra has made clear that their regulatory position statement (RPS) does not change the legal requirement for large producers to report their 2023 H1 and H2 data to the Environment Agency on or before October 1, 2023, and April 1 2024, respectively and “encourage obligated producers to use all reasonable endeavours” to do so. Two separate EPR reports will still need to be submitted.

Extended Producer Responsibility is one of the key projects which collectively form the Collection and Packaging Reforms (CPR) programme:

- Extended Producer Responsibility- UK-wide

- Deposit Return Scheme – England and Wales (separate for Scotland)

- Consistency in Recycling- England only

Why is EPR important?

EPR is designed as a fiscal stimulus to achieve higher packaging recycling levels. There is often a gap between the cost of collecting and recycling material and what the market is willing to pay for it. The gap is called the full net cost. EPR is designed for Producers to fund this gap to allow recycling to occur to levels that wouldn’t be achieved if left to the market.

The current system based on the purchase of Packaging Recovery Notes (PRNs) is a market-driven system and does not guarantee that this gap will be filled for each material stream or that the money will be distributed to where it is required.

The PRN system will remain until at least 2026/7 for all materials, but for household waste, an additional fee will be payable by producers to cover the full net cost of household packaging waste recycling from 2025.

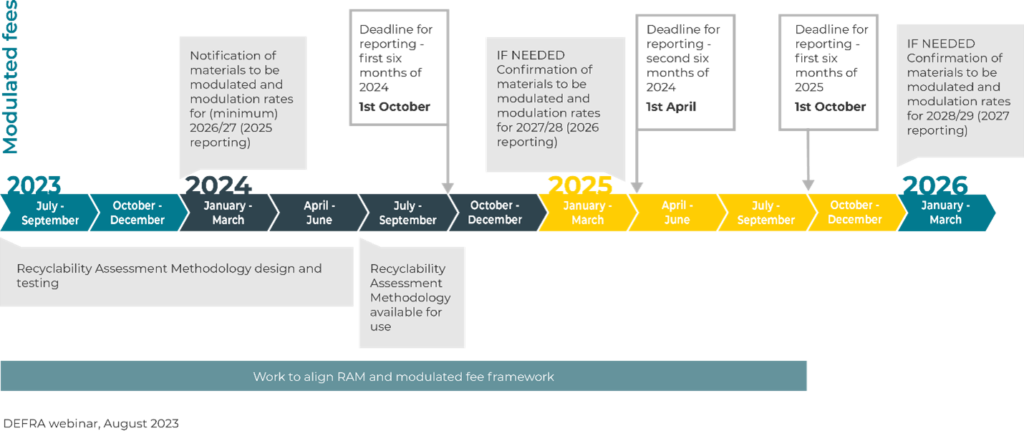

What are modulated fees?

A modulated fee system will be introduced in 2026, where varying compliance costs will be used depending on the environmental impact of the packaging placed on the market. For example, how widely recycled or recyclable a material is. This will require more in-depth data on the packaging materials than is reported in the current system. Packaging that can be easily recycled will attract lower EPR fees than hard-to-recycle packaging. Therefore, this will provide producers with a financial incentive to make their packaging more recyclable.

The government will hopefully start to provide some details on the structure of modulated fees towards the end of 2023. Nevertheless, hard-to-recycle materials will incur higher costs, whereas more easily recyclable packaging will be rewarded with lower fees.

Producers in the current system report the tonnage of packaging they have handled according to seven material categories (plastic, paper/card, glass, steel, aluminium, wood, and other). In the future, reporting will need to be done at a more granular level to enable the application of modulated fees.

Base Fees

For 2023 and 2024, producers will report packaging under eight broad material categories:

- Paper, card, fibre-based composites, plastic, aluminium, steel, glass, wood, etc.

- 2023 reporting will be used to generate illustrative fee rates for 2025/26

- Fees for the 2025/26 assessment year are based on 2024 reporting

- Any differences across materials simply reflect different LA disposal costs

Producer Fee

Year 1(2025/26)

Reporting year January- December 2024

Eight fee rates, reflecting the costs to Local Authorities of managing eight packaging materials at the end of life (base fees)

No modulation to incentivise producers to move away from less recyclable materials.

Year 2(2026/27)

Modulated fees applied

Reporting year January –December 2025

Material/formats to be modulated announced in winter 2023/24

More than eight fee rates (exact number to be determined) reflecting higher fees for less recyclable materials

Participatory design of the material list and the fee differentials.

The initial timeline for collating packaging data covers the period March 2023 – June 2023 (January 2023 – June 2023 if you have that data).

Upload and submit your data by 1 October. Compliance Schemes and producers will then be able to submit data from 13 September

**Large Producers

Defra has made clear that the Regulatory Positions Statement (RPS) does not change the legal requirement for large producers to report their 2023 H1 and H2 data to the Environment Agency on or before 1 October 2023 and 1 April 2024, respectively. No enforcement action will be taken if they are submitted by 31 May 2024.

Details on the structure of modulated fees towards the end of 2023.

2023 producers will report packaging under these 8 categories: Paper, card, fibre-based composites, plastic, aluminium, steel, glass, wood, and others.

Recyclability Assessment Methodology and Design and Testing.

Consultation on Draft Regulations (28 July and close on 9 October 2023)

Materials subject to modulation will have to be reported separately

Large producers will receive invoices for EPR fee payable across financial year 2025/26

Large producers will start to pay new EPR fee for household packaging waste

2023 reporting will be used to generate illustrative fee rates for 2025/26

Fees for the 2025/26 assessment year are based on 2024 reporting

EPR Fees based on 2024 data

Jan-March, confirmation of materials to be modulated and modulated fee rates for 2027/28 (2026 reporting)

April- June, Deadline for reporting second six months of 2024 data (1st April 2025)

Oct-Dec, Deadline for reporting second six months of 2025 data (1st October 2025)

Materials subject to modulation will have to be reported separately

Large producers will receive invoices for EPR fee payable across financial year 2025/26

Large producers will start to pay new EPR fee for household packaging waste

2023 reporting will be used to generate illustrative fee rates for 2025/26

Fees for the 2025/26 assessment year are based on 2024 reporting

EPR Fees based on 2024 data

Jan-March, confirmation of materials to be modulated and modulated fee rates for 2027/28 (2026 reporting)

April- June, Deadline for reporting second six months of 2024 data (1st April 2025)

Oct-Dec, Deadline for reporting second six months of 2025 data (1st October 2025)

Packaging data reflecting 2026/27 costs

Producers will need to label all packaging types except flexibles with ‘recycle’ or ‘don’t recycle’ by March 2026, with flexibles following in 2027. *likely to change

Modulated Fee System

PRN system will remain until at least 2026/7

Jan-March - confirmation of materials to be modulated and modulated fee rates for 2028/29 (2027 reporting)

Why is EPR being implemented?

In 2018, the UK adopted the Circular Economy Package (CEP), meaning that the UK is committed to the full net cost of collecting, sorting, treating, and recycling to be funded by producers rather than the market-based system currently being used. EPR switches the cost of funding household packaging waste collections from council taxpayers to producers; it is the UK’s answer to meeting the CEP, encouraging easy-to-recycle materials and penalising hard-to-recycle materials.

Does EPR affect your business?

If you are a producer first placing packaging on the UK market, whether UK-sourced or imported, it is likely you will be affected by EPR.

Extended Producer Responsibility (EPR) reforms include a number of new pieces of UK legislation. While other elements of the EPR reforms are being brought in over the coming years, some of the legislation has already taken effect as of 2023. Starting in 2024, reporting obligations under the EPR and the UK Packaging Waste Regulations will coexist.

Obligated producers classified as ‘large organisations’ with an annual turnover of greater than £2 million and who are responsible for supplying or importing more than 50 tonnes of empty packaging or packaged goods must meet the reporting requirement to give this data to the environmental regulator twice a year, starting from October 1 2023.

These producers will have to pay a waste management fee to the Scheme Administrator, which funds the collection of household packaging waste and buy packaging waste recycling notes (PRNs) or packaging waste export recycling notes (PERNs) to meet recycling obligations under EPR.

Producers will continue purchasing PRNs for household and business waste, but several major changes will occur. Firstly, there will be a single point of compliance for EPR costs, which will generally be the brand owner or importer of packaged goods. Secondly, a new system of ‘producer fees’ for household and on-the-go street bin packaging waste will be paid in 2025. These fees will be paid quarterly to a new Scheme Administrator set up to run the system. These fees will be in addition to PRNs and ensure that producers cover the full net cost of managing their waste. From 2026, these producer fees will be modulated based on the recyclability of packaging placed on the market. Rules ensuring packaging producers pay for the full net cost of household packaging, paid to local authorities, have been delayed from 2024 to 2025, but new data submission requirements for large producers by October 1 2023 and small producers by April 1 2024, remain in place.

‘Small’ producers, those organisations with an annual turnover between £1 million and £2 million and are responsible for supplying or importing between 25 and 50 tonnes of empty packaging or packaged goods throughout the UK, are liable to record and report data annually, but will be excluded from buying PRNs or PERNs, and paying administrative and waste management fees. Data should be recorded and retained from 2023, with submissions expected from 2025 (relating to 2024 data).

Due to the delay in the payment system for the EPR reforms until 2025, all businesses obligated under the EPR regulations will need to make submissions relating to 2023 data under both the new and old (2007) regulations in 23/2024.

What obligated businesses must do;

- Additional data on packaging type and recyclability will need to be gathered and reported every six months. By October 2023, the first report is due.

- Producers will be held more financially accountable starting in October 2025 for residential packaging waste.

- There will be a separate reporting obligation to report packaging supplied by UK nation.

- Beginning on April 1, 2026, every packaging (apart from flexible films) must have a recyclability label that reads “recycle” or “do not recycle.”

- Eco-Modulation fee – Further elements of Extended Producer Responsibility, including modulation of fees based on recyclability of packaging, payments for the management of litter and payments to businesses for the cost of managing packaging waste would be introduced in Phase 2, from 2025. The EPR fee invoices in 2025 will depend on the specifications of the packaging introduced to the UK market in 2024.

How much will EPR cost?

As soon as we can, we will indicate what your fees could be in 2025 (based on 2024 data).

From 2025 (fees payable in 2026), the waste management fee will vary depending on the type of materials you have reported. Your fee will be lower if you use materials that are easier to recycle.

When to collect and report your data for 2023

From January 2023, producers must begin collecting data to be retained and/or submitted. This data could include new requirements such as information about whether the packaging is classed as commonly placed in street bins, and evidence of where the packaging is likely to end up, the household or business waste stream. The first data submission was July 1 to October 1 2023 for large producers (>£2m turnover and >50t packaging), although no action will be taken as long as all data is submitted by 31st May 2024. Small producers should collect and retain data from Jan 2023, with submissions expected from 2025.

Large producers will have to report bi-annually on the type and quantity of packaging they place on the market, including a new material of fibre-based composites, using a single point of compliance (brand/importer), splitting packaging by layer and household and non-household and identifying if the materials are commonly littered. From January 2025, producers of household packaging will have to collect more comprehensive data for the introduction of modulated fees.

How to comply with EPR

To comply with the regulations, you must:

- Record data about all the empty packaging and packaged goods you supply or import in the UK from either January 1 2023 or March 1 2023 (for more information about this see the section about ‘when to collect and report your data for 2023’)

- Create an account for your organisation

- Pay a charge to the environmental regulator when required

- Report data about empty packaging and packaged goods you supplied or imported

When you report data, it depends on if you are a ‘small’ or ‘large’ producer, as detailed in the timeline above.

You may need to pay a penalty charge if you miss the deadline.

You may also need to report nation data.

When will EPR officially start, and what will the waste management fees for 2024 be?

The scheme for additional waste disposal payments has been delayed and is now scheduled to start in 2025 (based on packaging handled in 2024).

Defra says that the data it is currently collecting will provide the basis for establishing the packaging waste management fees individual producers will pay in 2025 and that more information on the fees will be provided ‘as soon as we can‘.

It had indicated that from 2026, the waste management fee will vary depending on the type of materials producers have reported. The fee will be lower for materials that are easier to recycle.

Packaging activities

You may need to act if you do any of the following:

What data will you need to collect?

You must collect data about the packaging you’ve supplied through the UK market or imported into the UK.

The data you collect must include the following categories:

- Packaging activity – this is how you supplied the packaging

- Packaging material and weight

- Packaging class – whether the packaging is primary, secondary, shipment or tertiary

- Packaging type – for example, if the packaging is household or non-household

There should be four parts to the data you collect about your packaging. These are:

You may also need to collect nation data. This is information about where your packaging has been sold, hired, loaned, gifted or discarded in the UK. Large organisations need to report data every six months. Small organisations report data once a year.

Find out if you’re a small or large organisation and what this means.

Reporting your data

Large organisations need to report data every six months. Small organisations report data once a year.

Find out if you’re a small or large organisation, and what this means.

You must report your data by submitting a file using the ‘Report Packaging Data’ service.

Find out how to create your EPR for packaging data file.

Check if you need to report nation data

Nation data is information about which nation in the UK packaging is supplied in and which nation in the UK packaging is discarded in.

If your organisation must act under EPR for packaging, you must submit nation data if you also do any of the following:

- Have a turnover greater than, or equal to, £1m and handle more than, or equal to 25 tonnes, of packaging

- supply filled or empty packaging directly to customers in the UK, where they are the end user of the packaging

- supply empty packaging to UK organisations that are either not legally obligated, or are classed as a small organisation

- hire or loan out reusable packaging

- own an online marketplace where organisations based outside the UK sell their empty packaging and packaged goods to UK consumers

- import packaged goods into the UK for your own use and discard the packaging

Data should be collected and retained for the 2023 calendar year, with submissions expected from 2025, relating to 2024 data.

Nation data should show where in the UK you’ve supplied packaging to a person or business who’s gone on to discard it.

Supplying packaging includes:

- selling

- hiring

- loaning

- gifting

This also includes packaging that you’ve imported, emptied and then discarded.

Penalties

If the deadline is missed, businesses may need to pay a penalty charge

Department for Environment Food and Rural Affairs (DEFRA) will establish a monitoring and enforcement regime where environmental regulators in England, Northern Ireland, Scotland and Wales will have the powers to monitor, audit and use civil and criminal penalties to drive compliance and address non-compliance.

Draft Regulations and what it includes?

The draft Producer Responsibility Obligations (Packaging and Packaging Waste) Regulations [2024] (“the draft Regulations”) set out obligations on producers to continue to collect and report data. These requirements mirror the requirements in the Data Reporting Regulations 2023 but with some further amendments to address small gaps in the data collection and reporting obligations.

For more details ref to the Draft Regulations click here.

Consultation on Draft Regulations

The government is seeking views/consultation on the “draft regulation” to ensure that the draft Regulations achieve the policy intentions set out in the Government Response, creating clear and operationally feasible obligations. Defra is managing the consultation process on behalf of government.

This consultation will run from July 28 and close on October 9 2023 and you can make sure your voice is heard by clicking here.

Getting help with EPR

We will be working with all our current clients on a one-to-one basis to prepare for the upcoming changes, but please do reach out to your account manager if you have any questions.

If you are new to the world of EPR, please speak to one of our advisors on +44 (0)1865 721375 to find out how we can help you take the complexity out of environmental compliance!

How to prepare for EPR?

To prepare for EPR and achieve a seamless transition to the new system, you should:

What is Ecoveritas?

The easiest and most comprehensive way to manage environmental data and reporting needs.

What does Ecoveritas do?

Ecoveritas is an EPR specialist, we provide a range of tools that allow you to simplify the data collection and reporting under EPR legislation in the UK and Globally.

To meet the complex challenges of managing EPR compliance reporting, Ecoveritas offers a unique combination of consulting, data and software that helps companies around the globe take the next step in their sustainability journey.

Our team takes a fresh approach to the EPR compliance market by adding years of supply chain and technical development expertise to an experienced environmental data team to provide SaaS-based services.

Our mission is to make it simple for companies to understand their obligations, gather the required data, submit reports and get compliant.

Ecoveritas’ services

- Extended Producer Responsibility Data Management & Reporting

- Plastic Tax Data Management & Reporting

- Global EPR Consulting

Ecoveritas can help you prepare your packaging for EPR and to get ready to record data from January 1 2023.

Navigating environmental legislation is time-consuming. For businesses operating across numerous countries, the issue is even more complex.

We can help;

- Identify how your business can best prepare to minimise EPR impacts

- Help you gather and capture the granular data EPR requires.