Plastic Packaging Tax

Ecoveritas is an environmental data specialist that provides a range of tools and expertise to brands, retailers and supply chains to efficiently minimise the environmental impact of their packaging.

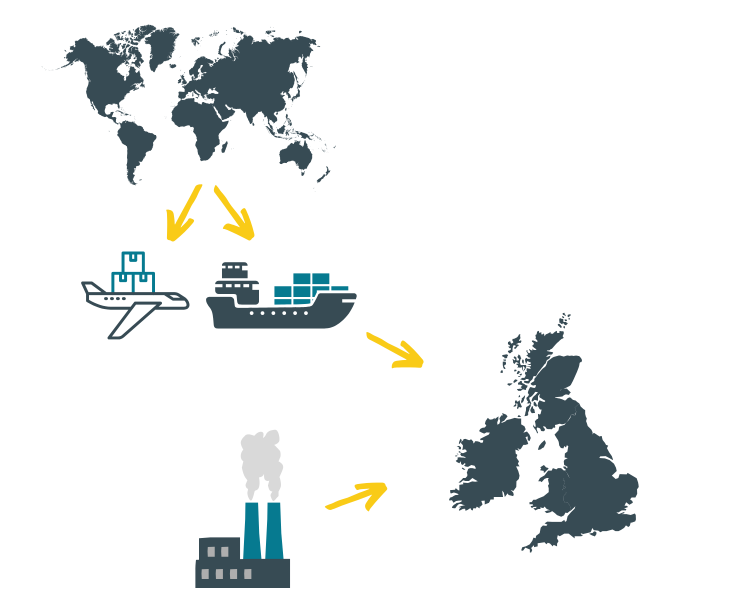

The Plastic Packaging Tax was introduced on 1st April 2022. The tax is designed to encourage the use of more recycled plastic and applies to plastic packaging produced in, or imported into, the UK that does not contain at least 30% recycled plastic.

The environmental tax forms part of the UK Government’s bid to tackle avoidable plastic waste and aims to drive real and lasting change in the packaging industry.

Registered companies will need to submit returns four times a year to HMRC.

How much is the tax?

The tax is charged per tonne and increases in April of each year. The tax is set at £223.69 from 1st April 2025.

Who does it affect?

Any business that produces or imports plastic packaging into the UK will be liable to pay the tax if the packaging contains less than 30% recycled content. Companies are exempt from paying the tax if they manufacture or import less than 10 tonnes of plastic packaging in 12 months.

If you identify that some of your plastic packaging is subject to the tax, you need to accurately calculate the weight to find out if you are liable and need to report.

If there are multiple operators in the manufacturing supply chain in the UK, the liable party will be the business that undertakes the last substantial modification before pack/filling.

The importer is defined as the company on whose behalf the packaging enters the UK, and/or the first company to commercially exploit it.

You need to register for the Plastic Packaging Tax if you:

- expect to import into the UK or manufacture in the UK 10 tonnes or more of finished plastic packaging components in the next 30 days

- have imported into the UK or manufactured in the UK 10 tonnes or more of finished plastic packaging components in the last 12 months

Information overload?

Don't worry- we know it can be a lot to digest. If you prefer, why not request a call back from one of our experts? We can guide you through all you need to know, at your own pace!

What are the reporting obligations under the UK Plastics Packaging Tax?

To comply with the UK Plastic Packaging Tax, businesses must submit a return on a quarterly basis. The reporting quarters run as follows:

- 1 April to 30 June

- 1 July to 30 September

- 1 October to 31 December

- 1 January to 31 March

Each return will request information on the weight of:

- chargeable plastic components the business has produced or imported

- non-chargeable plastic components the business has produced or imported

- chargeable plastic components where the direct export condition is not met

- chargeable plastic components produced or imported for which the direct export condition is met

- plastic components which are exempt because they meet the required threshold of 30% recycled content

- plastic components exempt as they are used for medicine.

Returns must be submitted and any incumbent tax liability paid by the last working day of the month following the end of the relevant accounting period. Businesses who calculate a nil liability will still be required to submit quarterly returns.

At what point does the Plastic Packaging Tax apply?

HMRC defines the plastic components as liable for the tax when ‘finished’. This is when the last substantial modification is made.

For plastic packaging that is imported into the UK and already contains goods or products, the tax applies to the packaging when they are imported, with no additional substantial modifications made.

The last substantial modification is the last manufacturing process that makes a significant change to the nature of the packaging component, as it alters one of the following characteristics of the packaging component:

- Shape

- Structure

- Thickness

- Weight

For other packaging, it will be the last substantial modification before the packaging is filled with products. This includes extrusion, moulding, layering, and laminating, forming, and printing. Not all manufacturing processes that change the shape or structure is considered as substantial modification. For example:

- Blowing or otherwise forming a packaging component from a preform;

- Cutting film to size or cutting formed trays out of a sheet;

- Gluing labels to a tub or heating a shrink film label onto a bottle;

- Sealing such as attaching a film lid onto a tub.

Who is exempt from the tax, and do they need to take any action?

There are four categories of packaging exempt from the tax. They are products:

Used for the immediate packaging of licensed human medicine

Permanently recorded as set aside for non-packaging use

Used as transport packaging to import multiple goods safely into the UK

Used in aircraft, ship and rail goods stores

Exempt packaging which counts toward the 10-tonne threshold for registration:

Plastic packaging used for human medicinal products, and plastic packaging permanently recorded as set aside for non-packaging use, must be included when working out the total weight of packaging manufactured or imported.

Exempt packaging which does not count towards the 10-tonne threshold for registration:

Plastic packaging used for transporting imported goods, and for stores on international aircraft, ship and rail journeys, does not need to be included when working out the total weight of packaging manufactured or imported.

What information should businesses be gathering for the tax?

The new tax calls for greater collaboration and transparency within the supply chain. The businesses that manage their data effectively will be able to maintain a clear audit trail and prove, without a doubt, the authenticity of the materials used in their packaging.

The tax returns will require information concerning the weight of:

- Chargeable plastic components that the business has produced or imported

- Non-chargeable plastic components that the business has produced or imported

- Chargeable plastic components where the direct export condition is not met

- Chargeable plastic components produced or imported for which the direct export condition is met

- Plastic components are exempt because they meet the required threshold of 30% recycled content

- Plastic components that are exempt through current PPT legislation

Once registered for the tax, you’re required to keep the records for at least six years following the end of each accounting period.

Notably, you should keep records even if you are below the threshold because of a rolling 12-month time period, so you could subsequently hit the limit and be liable to keep records and pay tax.

Trusted by industry leaders:

Partner with a specialist

Businesses should look to partner with a packaging data specialist that can consistently deliver a highly efficient and transparent service without the need to scale up to meet the requirements.

If you are new to PPT, please get in touch to find out how we can help you take the complexity out of packaging compliance!